R⋆STARS Data Entry Guide

R⋆STARS Data Entry GuideR⋆STARS Data Entry Guide

Chapter #2

System Processing Overview

This chapter provides a high-level overview of R⋆STARS’ functional accounting capabilities, systems profiles, and major processing subsystems used by Oregon.

2-2 Functional Accounting Capabilities

Pre-Encumbrance and Encumbrance Accounting

Expenditures, Disbursements, and Payment Processing

2-3 Application of System Profiles

System Management Profile - 97

Appropriation Number Profile-20

Program Cost Account Profile-26

Transaction Code Decision Profiles-28A/B

R⋆STARS has been designed to satisfy the requirements that are the responsibility of the agencies. These include basic accounting requirements, such as budgetary and general ledger accounting, and more sophisticated cost accounting requirements, such as program accounting, indirect cost accumulation and allocation, cash management, and grant accounting.

R⋆STARS provides for the integration of all information into a single, comprehensive system for planning, monitoring, and evaluating the performance of vital programs and projects. By integrating all of the major functional accounting requirements, the amount of manual intervention required to enter data, generate reports, and perform reconciliations is greatly reduced.

R⋆STARS has several components. An essential feature is the ability of different components of the system to interact with each other. Following is a brief explanation of each of these components.

A fundamental requirement of R⋆STARS is to capture and track budgets and to monitor obligations and expenditures against the available budget balance. The Appropriation Structure is used to monitor budgets for the Legislature and agencies. The Budget and Management Division of DAS controls the statewide structure for Appropriations. Appropriations (or Limitations) are the legal spending authority set by the State Legislature for each agency.

R⋆STARS has powerful and flexible budget capabilities. It provides very high-level budgeting information used by the Legislature and provides budgets at a more detailed level to State agency managers.

◾ The system allows different degrees of budget control.

◾ Controls can be set for programs, organization, funds, objects, grant, and projects.

◾ Budgets may be allotted to periods, such as months or quarters, to assist in program management.

◾ Expenditures, encumbrances and pre-encumbrances can be monitored against budgets at all levels.

◾ Revenues can also be budgeted for the “budget to actual” statement for the Annual Comprehensive Financial Report (ACFR).

There are four budget types in R⋆STARS. These budget types give the system the power and flexibility to accommodate the varying needs of State Government. They include:

◾ Appropriation

◾ Agency Budget

◾ Grant or Project Budget

◾ Financial Plan

To provide for the effective reporting of the appropriation and agency budget process, different types of appropriation actions, such as original and E-Board, are maintained separately in the system. Appropriations must be established at the start of the appropriation year so that control amounts are in place when the year begins.

The State obtains revenue from a wide range of sources and must maintain detailed information for effective accounting and control. Each agency is responsible for assuring its revenues are properly controlled and correctly recorded. Accrued revenues, receivables, cash receipts, and inter-agency transfers are all prepared, classified, and entered directly by the agencies. Actual revenues are compared to budgeted amounts, if the estimated revenues were recorded in R⋆STARS.

R⋆STARS can generate accounts receivable invoices, statements, and delinquent notices. It can calculate and record interest and/or late fees to delinquent accounts receivable documents based on user-defined parameters. If recorded and monitored, R⋆STARS will provide information on accounts receivable and their associated vendors.

R⋆STARS provides a full range of pre-encumbrance, encumbrance, expenditure, disbursement, and payment processing capabilities. Pre-encumbrance and encumbrance data can be recorded in the system on a document by document basis for all levels of the expenditure classification structure. Summary information is maintained in financial tables that reflect the effect of expenditure transactions against individual purchase orders, contracts, and other payments. As warrants are generated, the effects of disbursement transactions are recorded in the system tables for reporting and reconciliation. Each of the events in the expenditure cycle is described in the following segments.

Several important features exist in R⋆STARS to provide pre-encumbrance and encumbrance accounting capabilities. When encumbrances are recorded, R⋆STARS can automatically liquidate any pre-encumbrances previously recorded. The system automatically calculates the amount of the encumbrance liquidation associated with a specific payment. This is important because final payments of encumbered items are often different from the original encumbrance amount. When a final payment is different from the unliquidated balance of an encumbrance, within determined tolerance limits, the system can automatically generate a liquidation transaction equal to the document’s unliquidated balance.

The system controls pre-encumbrance and encumbrance transactions through a series of comprehensive fund control, profile control, and table look-up edits. The specific edits to be performed for a transaction are defined in the 28A/B – Transaction Code Decision Profiles. Transactions failing one or more of the system edits are reported either on-line or on the DAFR2151 Error Report with the appropriate error message(s).

Some encumbrance transactions are edited against available appropriation, agency budget, and allotment balances, depending upon indicators set in the 20 – Appropriation Profile and the 25 – Agency Control Profile. Based on specified options, encumbrance transactions that exceed the available budgetary balances will be either flagged as warning errors, fatal errors or ignored. Over-expending appropriations (and allotment thereof) can be cause for fatal errors. The type of control enforced on over-expending agency budgets is agency defined. Documents with warning errors are reported as such but will still post to the financial tables. Documents with fatal errors are not posted, but instead are held on the Internal Transaction File until corrected or deleted. In the last quarter of a biennium, Budget and Management Division of DAS has the allotment flag changed from warning to fatal for all agencies. This ensures that no agency will overspend for the biennium.

Additionally, R⋆STARS has edits which allow the system to determine if payments fall within specified limits of the amount originally encumbered. For example, a payment of $1,000 against an encumbrance of $500 will be identified as an error.

Expenditure accounting involves the proper classification of costs among the many categories required for governmental budgeting, accounting and reporting. Expenditures are generally recorded against a combination of agency, fund, object, and program structures. Within each of these structures, costs may be recorded at varying levels of detail. For example, some agencies may classify costs at the agency level, while others may classify costs at lower organization levels. Reports may be generated at each of the various levels within the agency, fund, object, and program structures. Additional reports are available that may include optional classification elements like grant, project, and agency codes 1, 2, and 3.

R⋆STARS provides for automated warrant writing. When payment voucher or vendor invoice data are recorded in the system, all of the data needed to generate a payment and remittance advice are stored in the system’s tables. Payments are scheduled using a due date. The system produces a warrant register each time warrants are produced. The payment processing cycle will automatically update the Accounting Event Table and other tables with the warrant number and issue date.

The D55 – Payment Processing Control Profile (see the Profile Maintenance Guide) defines how the system will sort payments. It determines how payments will be routed for distribution. There are 20 valid values available for payment sorting and routing. It defines remittance line printing for the remittance advice. This is done with the Remittance Sort Keys in the D55 Profile. There are 10 valid values available to define the number of lines printed and the information printed on each line.

The dollar amount on vouchers approved for payment is compared against available cash before the actual generation of payments. The system not only checks the available cash balance, but reserves it to prevent any subsequent transactions (i.e. cash transfers) from using the same cash.

Using the D55 Profile’s Sort Keys, the Expenditure Cycle allows consolidated payment of each agency’s multiple vouchers to the same payee, provides consistent reporting of payments made to payees, and supports federal tax reporting for 1099-MISC forms.

Agencies may request cancellation of warrants or checks when a record exists in the R⋆STARS Payment Control and Payment Cancellation and the agency has the warrant/check in hand. The Treasury will be notified by an R⋆STARS Interface to remove the warrant/check from their outstanding issue file. If the check is not on the R⋆STARS Payment Control and Cancel Tables (i.e. a Suspense Account check) and the agency wants to cancel a check, the agency must notify the Treasury directly with regard to the cancellation request.

The R⋆STARS general ledger accounting function maintains balances for the real, memo, and nominal accounts identified in the various funds’ account structures. This capability assists in managing, controlling and reporting on funds. The following are some primary objectives of governmental entities regarding general ledger accounting functions:

◾ Maintain a self-balancing general ledger for each fiscal entity to support GAAP reporting requirements.

◾ Ensure that the subsidiary ledgers are always in agreement with the control totals maintained in the general ledger.

◾ Properly account for revenue and expenditure transfers between funds.

One of the major purposes of the general ledger accounting function is to maintain control over the detailed records of a fund’s activities. One way this is accomplished is through the simultaneous posting of each accounting transaction to both the general ledger control accounts and the appropriate subsidiary accounts. R⋆STARS establishes a link between each subsidiary account at the control account level and generates system reconciliation and exception reports to indicate when and where an out-of-balance condition exits.

To provide maximum flexibility for management, general ledger accounting is performed at several levels of detail. The fund structure can be used for an example. At the highest level, the D20 – GAAP Fund Group Profile, general ledger control information is available for groups of funds, such as Governmental and Proprietary groups. Linked to the D20 profile is the D21 – GAAP Fund Type Profile i.e. General Fund, Special Revenue Funds, and Internal Service Funds. Within D21 GAAP Fund Types, the D24 – GAAP Fund Profile provides additional detail as required for the combining statements. The system provides for a self-balancing general ledger at the D24 profile level, D23 – Fund Profile level, and project and grant levels of detail. Similar hierarchical structures are available for the State Fund Structure (i.e. Appropriated Funds).

To permit reporting of the financial status and results of operations, R⋆STARS provides data that is fairly presented and of sufficient disclosure. This includes the proper classification of funds and maintenance of data on the accrual, modified accrual, or cash basis of accounting as required by law. Additionally, R⋆STARS provides for the proper recognition and treatment of accounting transactions for such things as inter-fund transfers and billings.

When an agency receives a Federal grant, or is involved in a Federal project; it often has to report on the status of that grant or project in a specialized format. Federal Fund reports present agency accountability on the use of Federal Funds. To comply with certain regulations, an agency may be required to generate financial data in the form of special reports. R⋆STARS can identify financial data by grant number. To facilitate the Federal audit process, detailed transaction reports are available to support the trial balance data.

R⋆STARS information for individual grants and projects can be maintained in a variety of ways. This includes the grant entitlement period, the federal fiscal year, or any unique accounting period that may differ from the system fiscal year. This reporting capability allows the system to maintain archive to date information as well as current year information.

R⋆STARS can maintain and report budget data applicable to individual grants, subgrantees, and projects. For example, it may be desirable to establish budgets for individual tasks or phases of a project and to track actual performance against these targets. R⋆STARS can record revenues on a grant and project basis and report these against expenditures, where applicable. It can account for and compare reported subgrantee expenditures to actual expenditures of the agency. Finally, the R⋆STARS’ data can be automatically converted to federal reimbursement categories (grant expenditure objects) to permit the generation of federal billing reports. Federal reimbursement invoices can be generated by a module called CMIA (Cash Management Improvement Act). This module of R⋆STARS is an automated billing system for specified grants based on various rates and clearance patterns. Comptroller object, agency object, or grant object can define rates charged in the CMIA module.

R⋆STARS can maintain a variety of data about each grant and project. These data include such things as the grantor, grant number, subgrantee number, type, category, object, Federal Grant Number, billing methods and schedules.

The agency maintained Recurring Transaction Subsystem has the ability to automatically post those transactions that occur periodically (i.e. monthly rental payments). The Recurring Transaction Subsystem includes the ability to define transactions that are generated on a pre-defined schedule, request proof lists, and to do the actual generation of transactions for a range of dates based on the schedule.

This subsystem can be used to define coding blocks and retrieve such coding blocks on-line on any financial transaction entry screen using a Recurring Transaction Index (RTI). The RTI can be input directly during transaction entry or can be looked up by the Program Cost Account (PCA) or Grant.

A cost allocation methodology may be required for agencies to prorate costs. The capability to allocate indirect costs supports the need to account for the full cost of specific segments of operations. Full cost allocation is also required to accurately account for reimbursement expenditures, particularly those reimbursable under federal grants. R⋆STARS cost allocation provides the following capabilities:

◾ Multiple cost allocation methods that allow agencies to distribute different types of indirect costs in different ways.

◾ Multiple data classification categories to distinguish allocated indirect costs from direct costs.

◾ Ability to determine the amount of indirect cost recoveries, to account for indirect cost variances, and to periodically allocate such variances.

The Report and Distribution Subsystem prepares the system’s financial reports. Most of the reports are developed from financial tables and profiles.

The objective of the reporting function is to fulfill the information requirements of accounting and management personnel. To meet these needs, the reports must display financial data at various levels of classification detail. Many of the reports provide the ability to change the level of detail based on the user-defined request.

All financial reports (which do not include system-generated control reports) are produced by user request. This allows the agencies to determine the frequency, timing, and time period of their agency’s reports. Additionally, agencies can use the system security capabilities to limit who can request reports and the data that can be reported.

Reports are discussed in detail in the R⋆STARS Report Guide which can be found at http://www.oregon.gov/DAS/Financial/AcctgSys/pages/ reportguide.aspx

To provide maximum flexibility in tailoring the system to meet the unique needs of the various state agencies, R⋆STARS is designed as a “profile-driven” system. This means the specific accounting structure and information processing logic is controlled through system profiles.

It is through the maintenance of these profiles, and not through modification to system software, that fiscal personnel control the accounting impact, the edits, and the profile updates associated with each input transaction. This frees the financial manager from dependence upon programming support to carry out changes in accounting structure, and provides substantial flexibility in responding to new and changing system requirements. Some of the system profiles used include:

97 |

– |

System Management Profile |

25 |

– |

Agency Control Profile |

20 |

– |

Appropriation Number Profile | 26 |

– |

Program Cost Account Profile |

24 |

– |

Index Code Profile | 22 |

– |

Cost Allocation Profile |

34 |

– |

Agency Vendor Profile | 52 |

– |

Systemwide Vendor Profile |

51 |

– |

Vendor Mail Code Profile | 27 |

– |

Project Control Profile |

29 |

– |

Grant Control Profile | 28A/B |

– |

Transaction code Decision Profile |

An overview of these above profiles is discussed below. Specific details for the each of these and other R⋆STARS profiles can be found in chapters #5 and #6.

SFMS Operations at DAS maintains this profile. By making simple on-line changes to this profile, SFMS Operations provides a system-level control over processing. To providethe control, the 97 profile maintains a variety of information regarding:

◾ Current Indicators such as Effective Date, Current Fiscal Year, and Current Month

◾ Last Closed Indicators such as Last Closed Fiscal Year and Last Closed Month

◾ Reporting Indicators which the reporting subsystem accesses to determine which reports to generate

◾ Control Indicators such as what is the Next Available Warrant Number and Direct Deposit Sequence

◾ Processing Cycle Information such as Current Cycle Number and Prior Cycle Number

R⋆STARS allows each agency to function independently. This means that decisions made by the accounting office of one agency regarding areas such as the level of control to be exercised over agency budgets need not affect the levels of control exercised by the accounting office of another agency. This flexibility is built into R⋆STARS through the 25 Profile.

The 25 profile contains a single record for each agency and fiscal year combination. This profile is created at the beginning of each fiscal year. For each agency, the profile provides the following information:

◾ Valid Agency/transaction year combinations used to control system functions.

◾ Document match level indicators that determine the required relationships between encumbrances and pre-encumbrances and their related liquidating transactions.

◾ Detail cost allocation processing rules, specific for that agency.

◾ Billing Deficit Coding Blocks to accumulate expenditure overruns for billable projects, if used.

◾ Billing Default coding Blocks to be used when required codes are not entered during transaction entry.

◾ Indicators that determine the effect of encumbrances and pre-encumbrances on agency budget controls.

◾ Indicators that determine whether an agency will capture fixed assets and associated threshold amounts.

◾ The last month and fiscal year closed.

◾ Reporting indicators to determine when to run monthly, quarterly, and annual reports.

In addition to the accounting classification data, the 20 profile contains several information elements. These include the effective dates of the appropriation and edit indicators that determine the type of control to be exercised. This table is normally created before the start of the appropriation year. The Budget and Management Division of DAS maintains this profile.

The 26 profile uniquely identifies each detailed program structure established by the accounting office at an agency. Program structure must be used in Oregon to meet budgetary requirements. The PCA serves three important functions within the system. First, it provides a simple coding reduction technique for referencing program information and other classification data. Second, the PCA contains an indicator that identifies to what program level that agency appropriations will be tracked. Third, the PCA is used to assist in the monitoring of direct and indirect costs for cost allocation.

Index is another coding reduction feature that focuses on the Organization Structure of an agency. The R⋆STARS classification structure provides up to nine levels of internal organizational classifications. Index Codes are assigned only at the lowest level organizations. Index has the capability to imply an Agency’s Fund Structure, Appropriation Number, Organization Structure, PCA, Agency Code, Grant and Project.

The cost accounting and reporting requirements of an agency have been fully integrated into the system structure. One method of integration is provided by the 22 profile. Through this profile, each agency can define how indirect cost pools are to be distributed to direct cost pools by cost allocation type. For each indirect cost pool, this profile defines the sequence (for step-down allocations), the allocation method, the distribution rates and base accounts for recording the allocations. All of these elements are used by the cost allocation subsystem to properly charge indirect costs to direct cost centers.

The system contains a vendor numbering capability that includes the ability to store multiple addresses for each vendor. Vendor information is used in the preparation of warrants, direct deposits and for other reporting purposes. Vendor number information is normally required by the system for recording accounting transactions such as disbursements. Vendors are defined in the 52 – Systemwide Vendor Profile, 51 – Vendor Mail Code Profile, and 34 – Agency Vendor Profile. In Oregon, the 34 profile is agency defined and is being used for customer numbers for billing purposes.

The 27 profile is the focal point for the editing of project related transactions and for the preparation of bills for project related expenses. The 27 profile provides the ability to define unique project accounting structures for each agency’s projects. Information elements contained in the profile provide additional accounting classification data, as well as several indicators that control the processing of project related data. An optional billing segment, used by the billing program, identifies the billing cycle, method, rates, base, and other billing data.

The 29 profile is very similar to the 27 Profile. The 29 profile provides substantial flexibility in the methods used to identify and account for grants. To provide this flexibility, this profile maintains a variety of information regarding each individual grant, grant type, billing method, posting indicators, control dates and a number of other classification elements.

The 28A and 28B profiles determine the accounting impact (debits and credits) of each financial transaction entered. They determine which data elements are required, optional, or not allowed on each transaction. There must be a Transaction Code (T-Code) established for each type of accounting transaction to be processed in the system.

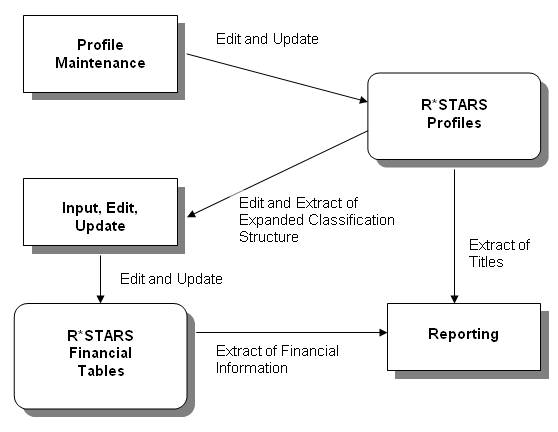

In the past, accounting systems often consisted of many independent modules, with each module designed to support a single functional accounting area. Many of these modules were developed as a result of the identification of a specific information requirement and the development of an isolated set of programs to satisfy that need. Systems designed in this manner were generally characterized by limited integration, redundant and inefficient system processing, and limited flexibility. R⋆STARS has been designed to overcome these deficiencies. The accounting logic in R⋆STARS is defined in the system profiles. There are few system modules that directly support a single functional accounting area. Instead, each module supports the processing requirements of all functional accounting areas. R⋆STARS is composed of three major processing modules:

◾ Profile maintenance. (Discussed in the Profile Maintenance Guide.)

◾ Input, edit, and update (which incorporates financial transaction processing, document tracking, and payment processing). (Discussed in the Date Entry Guide.)

◾ Reporting . (Discussed in the Report Guide.)

Each module is fully integrated and capable of capturing, transmitting, recording and reporting the transactions handled daily. The modules are depicted in the drawing below.

The profile maintenance module performs all maintenance functions for the system profiles. There is a single maintenance program for each of the system profiles. The following maintenance functions are performed by each of these programs using specified function keys:

Add |

– |

create a record. |

Change |

– |

alter the content of a record. |

Delete |

– |

remove the record. |

Recall |

– |

retrieves a specific record. |

Next |

– |

retrieves the next record. |

For each profile, the ability to perform these functions is controlled by system security. This helps ensure that only valid profile maintenance activities are performed.

The input, edit, update process (IEU) is the focal point for all financial data entering R⋆STARS. The following basic processes are performed:

◾ Data Input and Classification: Accounting transactions entering R⋆STARS may be received directly from users, from other subsystems, or through the standard interface procedure.

◾ Data Edit: The transactions are edited in accordance with certain edit rules. If the accounting transactions pass the required edit tests, they may then update the financial tables. If they fail any of the required edits, the errors must be corrected before they can update the tables.

◾ Error Correction: Batch transactions found to be in error by the input, edit, or update process are not rejected from the system, but instead are placed on the Internal Transition file. Accounting personnel may then recall the transactions in error and correct the specific field(s) in error.

◾ Payment Processing: This function is an integral component of the core input, edit, and update process. Payment processing generates warrants for approved payable transactions.

The Financial Table Update program performs fund and financial table control edits and then posts the valid transactions to the financial tables. These table updates are performed based on the posting indicators retrieved from the 28A/B profiles. Updates to the edits and tables can be performed in batch or on-line.

In batch, when a transaction fails certain types of edits, the transaction is written to the Internal Transaction file with edit mode 3. The transaction is not posted to any of the financial tables. Some edits may be established as warnings only, in which case the transactions would be allowed to post to the tables, but are flagged with warning messages.

Transactions that do not pass fatal edits when entered on-line with edit mode 2 must be corrected on-line before they will post.