Processing Timeline

Upon receipt of your form, please allow 2-3 weeks for processing.

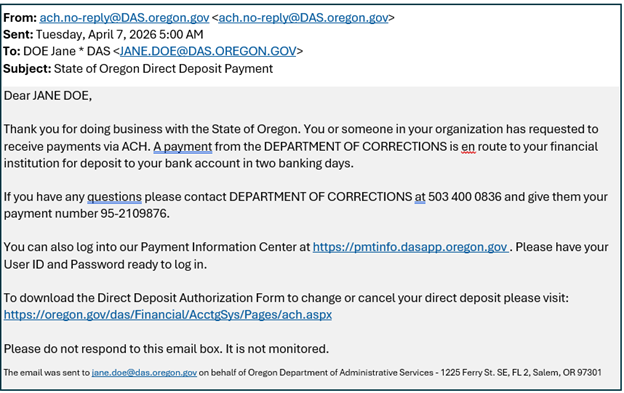

After we process your form, you will receive an email the next day similar to the one shown below:

How Direct Deposit Payments Work

Direct deposit payments are issued by the paying agency from R*STARS. The payment takes two banking days to reach your bank account. If funds do not appear on the deposit date, contact the ACH Coordinator.

Payment Information Center

When a direct deposit payment is processed, you'll receive an email similar to the one shown below with instructions to log in to the Payment Information Center to view remittance details:

For direct deposit payments, all remittance details are available in the Payment Information Center instead of being printed on a warrant or check. Through the Payment Information Center, you can:

- View up to 18 months of payment history

- See full remittance details for each payment

- Verify payment dates and information

Important Details:

- You will receive a User ID by email after your direct deposit account is set up.

- You must create a password

- For User ID help, contact the ACH Coordinator.

Bank Statement Notes

For simple, one line transactions, some payment information may appear on your bank statement.

If multiple payments are combined, your statement will show:

“SEE HTTPS:--PMTINFO.DASAPP.OREGON.GOV FOR TRANSACTION DETAILS.”

Questions

For questions about payment amounts or payment status, contact the paying agency listed on your remittance details.

For questions about electronic transmission or direct deposit setup, contact ach.coordinator@das.oregon.gov