The Oregon Public Employees Retirement System (PERS) was established in 1946 as a retirement benefit for public

employees in Oregon (i.e., people who work for Oregon state, county, or city governments). More than 900 state

agencies,

public schools, community colleges, and local governments (cities, counties, and special districts) participate in

PERS,

which covers about 95% of public employees in Oregon — more than 420,000 people.

The system gives PERS retirees a pension and an Individual Account Program (IAP) account. The pension provides

monthly

payments for life, and the IAP provides payments until the account balance reaches zero. For both programs, retirees

have options for how they want to receive their benefits.

To read definitions of any of the terms used on this webpage, refer to the employers’ Glossary quick-reference guide.

How PERS works: Legislature, Treasury, and PERS

The benefits provided by PERS, the system, are decided by the Oregon Legislature. The program is funded by

interest

earned on the Oregon Public Employees Retirement Fund (OPERF), employer contributions, and member contributions.

The

funds are collected by PERS, the agency; managed by Oregon State Treasury; and invested by the Oregon Investment

Council.

Watch the video “How Does PERS Work?” to understand how these entities

work together to manage PERS.

Legislation impacting PERS

As the plan sponsor for Oregon’s public pension program, the Legislature defines the eligibility rules and

benefits

of PERS by making changes to Oregon laws (Oregon Revised Statutes). To look up past and present legislative

changes to

PERS, go to the Legislation Impacting PERS

webpage

and choose the year a bill was signed into law.

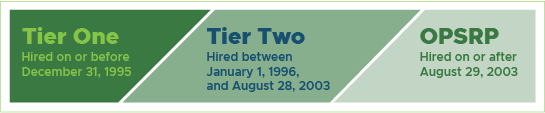

Three pension programs: Tier One, Tier Two, and OPSRP

PERS is divided into three pension programs: Tier One, Tier Two (both detailed in

Oregon Revised Statute (ORS) Chapter

238), and the Oregon Public Service Retirement Plan (OPSRP)

(detailed in ORS Chapter 238A). Tier

One and Tier Two are both closed to new members; all new employees are eligible to become members of OPSRP.

The program a member is in is determined by their hire date.

A member remains in their program unless they lose membership or withdraw from PERS. Even if they retire and then

return

to work for a PERS-participating employer, they stay in their original program. If an employee moves to a

different

PERS-participating employer, they remain in their program and continue to build their benefits.

Tier One

Tier One is the oldest and most generous PERS plan. Tier One retirees receive a pension, an IAP, and a member

account.

Some members also have a variable account (optional). Tier One retirees generally earn more benefits than Tier Two

or

OPSRP (see the Benefit Component Comparisons

Chart).

Tier Two

Tier Two was created by the Oregon Legislature to be less costly for employers than the Tier One plan. However,

over

time, it did not reduce costs enough. Employers continue to pay a higher contribution rate for their Tier One and

Tier

Two employees than their OPSRP employees.

Oregon Public Service Retirement Plan (OPSRP)

In 2003, the Legislature gave PERS a major overhaul and created the Oregon Public Service Retirement Plan. Over

time, as

more people retire under the OPSRP plan and fewer retire under Tier One/Tier Two, employers’ PERS costs will go

down.

PERS membership: gaining, maintaining, and losing

Becoming a PERS member

To become a PERS member, an employee must complete a wait time (aka waiting time, waiting period, or trial period)

of

employment that satisfies these rules:

- Six months of uninterrupted service (i.e., no break in service of 30 or more consecutive working days).

- The employee is still working for the same employer at the end of the six-month period.

- The employee is still working for the same employer on the day after the six-month period ends.

Vesting

To vest their PERS membership, an employee must work for five years in a PERS-qualifying position for at least 600

hours

per year. The years do not need to be consecutive, but the employee cannot have a gap in qualifying employment of

more

than five years. Once a member is vested, the only way they can lose their PERS membership is if they withdraw.

Learn

more about membership withdrawal on the Withdrawal Information webpage.

All current members of Tier One and Tier Two are already vested because they have worked at least five years.

An OPSRP member becomes vested in OPSRP when one of the following occurs:

- The member completes at least 600 hours of service in each of five calendar years.

-

The member reaches normal retirement age. For a list of normal retirement ages for each job classification, go

to

employer

reporting guide 1, Overview of PERS,

section “Types of PERS Retirements,” “Normal Retirement.”

Maintaining membership (loss of membership)

To maintain membership in PERS, a PERS member needs to work in a “qualifying” position (i.e., more than 600 hours

of

service per calendar year).

Membership in PERS is portable, meaning a member who leaves one PERS-participating employer to work for another

PERS-participating employer retains their membership and continues to earn benefits.

The only way a PERS member can involuntarily lose their membership is if they are not vested and they work fewer

than

600 hours/year for a PERS-participating employer (or stop working for any PERS-participating employers) for five

years

in a row. When that happens, they enter loss of membership (LOM) status, which cannot be reversed. They can

withdraw

funds that they contributed from their salary but may not receive funds contributed by their employer. If a person

in

LOM status enters PERS-participating employment later, they can establish a new membership after serving a

six-month

wait time. Members can learn more about LOM on the Member Annual Statements:

Loss of Membership FAQ webpage.

Withdrawing membership

A PERS member can voluntarily end their membership and withdraw their IAP funds by submitting a member account

withdrawal application. Withdrawing funds from any PERS account before retirement withdraws membership from all

PERS

plans, meaning the member forfeits their membership, all service credit, and their pension.

Learn more on the Withdrawal Information webpage.

A vested PERS member who stops working for a PERS-participating employer does not need to withdraw. They can leave

their

accounts with PERS for the rest of their career; they will still receive pension benefit payments when they

retire.

Important factors for your employee to consider when deciding whether to withdraw their member account(s):

-

Oregon law requires that members who withdraw from any PERS plan withdraw from all PERS plans in which they

participate.

-

If you are vested and you do not withdraw your member account(s), you will be eligible for lifetime monthly

benefit

payments at retirement — no matter how many years pass without you working for a PERS-participating employer.

Learn more

Withdrawal Information webpage

Senate Bill (SB) 1049 and OPSRP Withdrawals webpage

Retiring from PERS: job class, service, age

PERS members must reach a particular age to be eligible to retire and begin receiving their PERS retirement

benefits.

The particular age is determined by:

- Their PERS program (Tier One, Tier Two, or OPSRP).

-

Their job classification (e.g., General Service, Police and Fire, School Employee).

For a complete list of job classifications, go to the Job

Classification Codes guide.

- How long they have worked for a PERS-participating employer (in certain job classes, members can retire once

they reach 25 or 30 years of service, no matter their age).

Learn more

Tier One/Tier Two Steps to Retire webpage

OPSRP Steps to Retire webpage

Employer

reporting guide 16, Reporting a Retirement

PERS accounts: tracking and updating

Member annual statements

Every spring, PERS mails annual statements to all active PERS members and inactive members who still have a PERS

account. The statements list the member’s service credit, IAP account balance, and Employee Pension Stability

Account

(EPSA) balance, when applicable. If they are Tier One or Tier Two member, they may have a regular account and a

variable

account. If they are a Police and Fire member, they may have a unit account.

The Member Annual Statement FAQs webpage provides

links to interactive examples of statements for Tier One, Tier Two,

and OPSRP.

Online Member Services (OMS) tool

PERS members can view their account information anytime using the OMS tool. You can direct members to the What is OMS?

webpage to read what active, inactive, and retired members can do in OMS.

Divorce

If a member gets divorced, their PERS benefits may be affected. When your employee gets divorced, they need to

submit a

copy of their divorce decree and other authorized forms to the PERS Divorce Unit. In addition, Tier One and Tier

Two

employees may want to change their beneficiary information if their divorce decree allows. Members can learn more

on the

Divorce webpage.

Death and beneficiaries

A portion of some members’ PERS benefits can be left to a beneficiary when they die. How much can be left and to

whom

varies based on which PERS program the member is in, whether someone died before or after retirement, and the

beneficiary choices they make.

Learn more

Designating a Preretirement Beneficiary webpage

Member Death for Tier One/Tier Two webpage

Member Death for Oregon Public Service Retirement Plan (OPSRP)

webpage