Overview

When you, an employer, make a lump-sum payment to prepay all or part of your pension unfunded actuarial liability

(UAL), the money is placed in a special account called a “side account.” This account is attributed solely to the

employer making the payment and is held separately from other employer reserves. The money is invested in the

Oregon Public Employees Retirement Fund

(OPERF) and is subject to earnings and losses.

Expiration of side accounts in 2027

A significant number of employer side accounts* will reach their 20-year end date on December 31, 2027. This means

that by that date, 182 side accounts opened by 143 employers between 2002 and 2007 will no longer provide a rate

offset.

PERS Actuarial Services is working with employers to help them through the 2026–2028 side-account expiration process,

which is explained in this section. Throughout the process, PERS Actuarial Services will:

- Track side account balances every month.

- Inform employers if their accounts will run out of funds before the end date of December 31, 2027.

- Offer options to employers whose accounts will have a positive balance on the end date.

- Provide informational materials and online sessions to ensure employers are informed and supported.

The sections below explain the two or three statuses a side account will go through, the

major milestones occurring in 2027, and the complete process and schedule.

The schedule includes a printable diagram version.

*The percentage is between 40% and 50% of all side accounts. Actuarial Services cannot give an exact percentage

because it decreases as employers open new side accounts.

Three side account statuses: amortized, expired, closed

On its journey to its end date on December 31, 2027, a side account can go through three statuses (which are

explained in detail in this section):

- If an account runs out of funds early, it is in

amortized status. If this happens, the offset stops on the first day of the following month.

The employer is invoiced for any negative balance in June 2027.

- On the June 30, 2027, expiration date, a 2027 expiring side account reaches

expired status.

Offsets stop. If the account has a small positive balance that is being

credited to the employer, that credit takes place.

- On December 31, a 2027 expiring side account reaches

closed status.

There is no more activity on the account past this date other than final

reconciliation. If the account has a large positive balance that is being transferred to another side account,

that transfer takes place.

Details of each status are below.

Amortized account

This is an account that has run out of funds before its expiration date. If an account reaches amortized status

before it expires, it will remain open but inactive, as described in this section. This usually causes a negative

balance because the balance is unlikely to hit exactly $0.

Here are the rules for an account that has reached amortized status.

End date: An amortized account retains its original end date of December 31, 2027.

Preventing a negative balance: Actuarial Services cannot stop amortizations before your account

goes negative. Only a zero or negative balance before the expiration date can stop amortizations (aka rate

offsets).

Receiving annual earnings: All side accounts receive a proportionate share of earnings crediting

at year-end.

Explanation: Side accounts are subject to earnings or losses at the end of the year, whether their

balance is positive or negative. All side account funds are invested in the Oregon Public Employees Retirement

Fund (OPERF), and earnings are applied as a whole to every reserve in the fund. This is per

Oregon

Administrative Rule (OAR) 459-007-0530, Crediting Earnings to Employer Lump-Sum Payments.

Stopping the rate offset: When the account hits $0 or less, the offset stops on the first day of

the next calendar month.

Reconciliation of amortized account: In April 2027, Actuarial Services reconciles or "trues

up" accounts that amortized in 2026.

If you have a 2026 amortized account, in June 2027, you are invoiced for any negative balance through your EDX

statement. The charge appears on your invoice as "PERS Prior Yr Undr-Remitted Cntrb" in the Invoices

subsection of the Pension section of your statement. There is no penalty or extra charge for overdrawing funds.

Learn more about finding this section of your statement in

employer

guide 26, Understanding Your Statement

Paying the side account admin fee: A side account that provides an offset for at least one

calendar month of the calendar year is charged the $500 admin fee for that year. The fee is charged at the end of

the year and comes out of annual earnings.

Expired account

Side accounts expire on June 30 of their expiration year, which is usually 20 years after the account was opened.

As of that date, the account is expired. The rate offset stops the next day.

Here are the rules for an expired account.

Stopping the rate offset: The rate offset stops on July 1 of the expiration year (six months

before the December 31 end date).

Retroactive pay dates: After the expiration date, if you report pay for a date before the

expiration date, you do receive an offset on that payroll. For example, on August 1, if you report payroll from

May 1, you will receive offset on that payroll.

Handling nonzero balance: Upon the account's expiration, any projected outstanding negative

or positive balance is handled as explained below. Accounts that amortized in 2026 are included in the negative

category.

NEGATIVE: for accounts that have a negative 06/30/2027 projected balance.

On the expiration date of June 30, 2027, the account reaches expired status. The rate offset stops the next day.

POSITIVE: for accounts that have a positive 06/30/2027 projected balance.

The employer will receive the balance. How and when you receive it depends on the size of the balance.

- Balance of up to 34.99% of payroll receives CREDIT. If the account's June 30, 2027, projected balance is

less than 35% of the payroll reported in your most recently published valuation report, the employer will

receive a credit of the balance by the end of June 2027. (Valuation reports are available on the

Actuarial Valuations webpage.)

-

Balance of 35% of payroll or more receives OPTION FOR TRANSER TO ANOTHER SIDE ACCOUNT. If the

account's June 30, 2027, projected balance is 35% or more of the payroll in its most recently published

valuation report, the employer can choose between receiving a credit or rolling over the balance to a new or

existing side account.

The fine print

- 1. Employers must inform Actuarial Services of their choice by

May 31, 2027.

- 2a. If you choose to deposit funds into a

new side account, be aware that, in accordance with

OAR-459-009-0086,

the minimum lump-sum payment required to establish a new side account is the lesser of:

- 25% of the individual employer's unfunded actuarial liability (UAL).

- $250,000.

- 2b. If you choose to deposit funds into an existing side account, be aware of the following:

- You may not make more than two additional deposits into a side account in a calendar year.

- Adding funds to an existing side account does not affect the amortization period of the account (i.e.,

its original end date remains the same).

- Any change to your contribution rates caused by the deposit will be effective on July 1 of the calendar

year following completion of the actuarial valuation for the year in which the additional deposit is

made.

Closed account

In the year an account expires, it is considered 'closed' on the last business day of the calendar year.

Once an account is closed, no side account transactions are processed regardless of the payment date. After the

side account closes, final reconciliation activities bring the account to zero. Once that is completed, the

account closing is finalized.

Closing date for 2027 expirations: For accounts that expire in 2027, the closing date is December

31, 2027.

Reconcile or "true up" the account: In June 2028, PERS Financial Reporting Section does

final account reconciliation. You are invoiced for any negative balance, earnings, or applicable administrative

fees remaining from the account(s) that closed in the preceding calendar year.

2027 milestones

In April — PERS Actuarial Services reconciles any side accounts that amortized in 2026. Employers

are billed for any negative balance in June.

In May — PERS Actuarial Services performs two calculations on side accounts that have not yet

amortized:

- Actual balance as of 12/31/2026.

Projected 06/30/2027 balance: What the balance is projected to be on June 30, 2027 (the expiration date).

See April 2027 under "Side Account Expiration Process and Schedule" for details about this

calculation.

If projected balance is

less than 35% of the valuation payroll from their latest actuarial valuation report, they

will have the balance of their side account credited to them on June 30.

If the projected balance is

35% or more of the valuation payroll from their latest actuarial valuation report, they

will have

two options for receiving the balance of their side account: it can be credited to them or

rolled over into another side account — either an existing side account or a new side account — at the end

of the year.

May 31 — Deadline for employers with 35%+ accounts to inform Actuarial Services of their choice

between credit or transfer to new/existing side account.

In June — Funds transfer out of accounts that are being credited to the employer. Funds remain in

accounts that will be transferred to a new or existing side account on December 31. Employers with amortized

accounts are billed for any negative balance.

July 1 — New rates for 2027-29 biennium go into effect for all employers. Rate offsets cease for

all 2027 expiring side accounts.

November 1 — Milliman completes new side account calculations for employers who are opening new

side accounts.

December 31 — Remaining balances roll over into new or existing side accounts. All original 2027

expiring accounts close. New side accounts will open the next day.

Side account expiration process and schedule

This section presents two different ways to learn and keep track of the side account expiration process.

Choose one or both to suit your learning style.

- Click the image below to open, download, and/or print the four-page

2027 Side Account Expiration Schedule diagram (PDF).

- Scroll down to “Schedule” to read a description of all side account events occurring in 2026, 2027, and 2028.

2027 Side Account Expiration Schedule diagram

Click the image or paste

https://www.oregon.gov/pers/emp/Documents/Misc-Documents/2027_side_account_expiration_process.pdf

into your browser.

Schedule

This section details what will take place as side accounts approach their end date. For a graphic layout of this

schedule that you can download and print, open the

2027 Side Account Expiration

Schedule Diagram.

2026

Every month: PERS Actuarial Services tracks side account balances.

If account amortizes: If a side account reaches or is about to reach amortized status, Actuarial

Services notifies the employer. The rate offset stops on the first day of the next calendar month. Accounts

that amortize in 2026 are reconciled in 2027.

August 25: Actuarial Services holds an online information session to explain the side account

expiration process and allow employers to ask questions. (Invitations and links coming by News Bite emails.)

September 25: Milliman presents the new 2025-27 employer contribution rates to the PERS Board for

approval. (Information about the meeting will be on the

PERS Board webpage.) After rates are approved, the

system-wide valuation report and list of new net contribution rates for all employers are published to the

Actuarial Valuations webpageand

Contribution Rates webpage, respectively.

September 29: Actuarial Services holds a second online information session to explain the side

account expiration process and allow employers to ask questions. (Invitations and links coming by News Bite

emails.)

October: Employer 2025 rate-setting valuations are published on the

PERS Actuarial Valuations webpage. Valuation

reports include system-wide and individual employer 2027-29 contribution rates and the data used to calculate

them.

2027

April:

- All side accounts receive 2026 earnings or losses.

- Actuarial Services reconciles all amortized side accounts. Employers are invoiced for negative balances in

June.

Financial Reporting performs two calculations on expiring side accounts that are not projected to be

amortized before June 30, 2027:

a) Actual 12/31/2026 balance.

b) Projected 06/30/2027 balance.

Below is an example of how the projected balance is calculated.

May: Employers are notified of their side account projected balance and options.

- Smaller balances will receive a credit: If the projected balance is less than 35% of the valuation payroll

reported in the employer’s most recently published actuarial valuation report, the employer will receive a

credit on the expiration date.

- Larger balances can choose credit or rollover to another side account: If the projected balance is 35% or

more of the valuation payroll reported in the employer’s most recently published actuarial valuation report,

the employer can choose between credit or transfer to a new or existing side account.

Options for receiving balance in the account, based on June 30, 2027, projected balance

| If fund has | And amount is specifically | Then employer can receive balance as |

|---|

| Smaller balance | Less than 35% of payroll from most recent valuation report | Credit only |

| Larger balance | 35% or more of payroll from most recent valuation report | Either credit to their reserves or transfer into a new side account or existing side account (for rules, see “The Fine Print”) |

May 31: Deadline for employers with larger balances to inform Actuarial Services of their

selection of credit or transfer to another side account.

June:

- Employers who are receiving their positive side account balance as a credit receive their credit by the end

of the month.

- Employers who have a side account that amortized in 2026 are billed for any negative balance on the EDX

invoice. The charge appears on your invoice as “PERS Prior Yr Undr-Remitted Cntrb” in the Invoices subsection

of the Pension section of your statement.

- Employers who are receiving their positive side account balance as a transfer to another side account do not

receive the balance until the end of the year.

July 1: New 2027-29 employer contribution rates go into effect.

Rate offsets cease for all 2027 expiring side accounts.

-

Accounts that had their balance credited: These accounts remain in expired status until they

close at the end of the year.

-

Accounts that will have their balance transferred to another side account: Actuarial Services

calculates the accounts’ actual balances as of 6/30/27 and shares with employers. Accounts are expired;

balances remain in accounts until they are transferred to another account at year-end.

September 30: Deadline for employers who are opening a new side account to request a new side

account calculation from Milliman.

November 1: Milliman completes all calculations and provides information to Actuarial

Services.

November 10: Deadline for Actuarial Services to notify new/existing side account employers of

their new 2028 offset rates.

December 31: Positive balances transferred to new and existing side accounts. All 2027 expiring

side accounts close.

2028

January 1: New offsets begin for new side accounts.

April: All closed side accounts are reconciled.

June: Following earnings crediting for calendar year 2027, any applicable resulting invoices or

credits are processed.

Benefits of a side account

Side accounts increase an employer's actuarial assets, reducing the gap between actuarial assets and

actuarial liabilities. When liabilities exceed assets, this becomes a UAL. (To learn more about UAL, read “Guide to Understanding UAL.”)

Establishing a side account reduces your pension obligation, which reduces your employer contributions and rates

over time.

How to establish a side account

If you are interested in establishing a side account or have additional questions, please email

PERS Actuarial Services.

Employers have two options for establishing a side account:

- Request an actuarial calculation.

Requesting an actuarial calculation allows for an immediate rate offset. Employers can select the

first of any month within a rolling 12-month period for their rate to begin.

An actuarial calculation costs $1,000 for one date and one payment amount. Each additional date,

payment amount, or amortization schedule (if applicable) is an additional $250.00.

- Receive the rate offset effective July 1, following the publication of the actuarial valuation of that year.

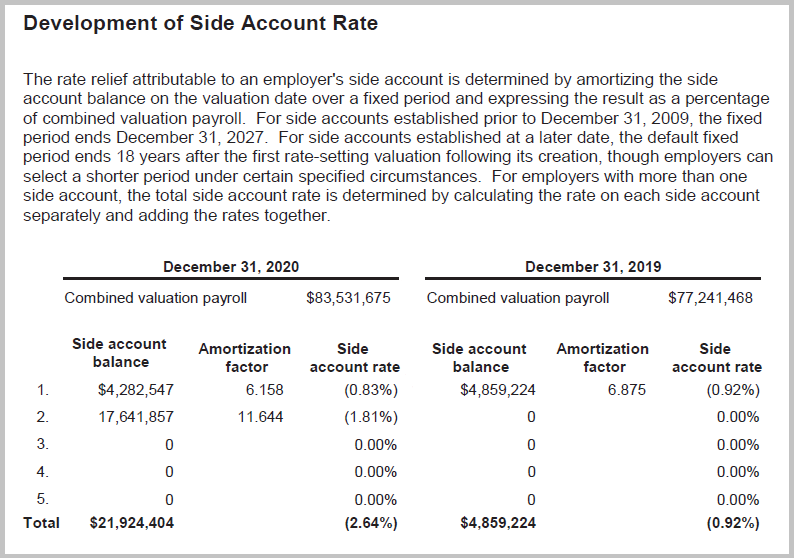

How the side account offset rate is calculated

The side account rate offset is recalculated during each biennial rate-setting actuarial valuation. The new side

account amount is determined by deducting the money that was transferred to the employer's reserves to reduce

their monthly statement (along with the annual maintenance fee). The gains or losses are added to the total side

account amount. This information is available in your actuarial valuation.

Example from an actuarial valuation.

Once the new side account amount is established, the PERS consulting actuaries use the formula below to calculate

the new side account rate offset:

Total lump sum ÷ combined valuation payroll ÷ amortization factor =

Side account rate offset

Example from an actuarial valuation.

To estimate the effect of a side account, please use the

Employer Rate Projection Tool.

Administrative fees

Side accounts are charged an annual fee for their administration. The fee is $1,500 in the first year and $500

each subsequent year. The fee is automatically taken out of your side account when earnings are applied.

An actuarial calculation costs $1,000 for one date and one payment amount. Each additional date, payment amount,

or amortization schedule (if applicable) is an additional $250.00.

Amortization options

Side accounts are typically amortized over 20 years. However, as established with

Senate Bill 1566 (2018) and Senate Bill 1049

(2019), employers making a lump-sum payment of at least $10 million can elect an amortization period of 6

years, 10 years, 16 years, or 20 years. They can also choose to defer their rate offset date beyond the standard

rolling 12 months. These amortization options require an actuarial calculation.

Side accounts for pool members

Although employer rates are set at a pool level, employers have the option to establish a side account to

differentiate their individual rate.

For State and Local Government Rate Pool (SLGRP) employers: The supplemental payment is first

applied toward your transitional liability, if you have any, and the rest is placed in a side account.

For School District Pool members: Once you create a side account, you start to receive your own

valuation, which contains full details on how the side account rate is calculated and the amount in the side

account. Additionally, the valuation contains information that is specific to you, the employer, including

combined valuation payroll and the UAL allocated to the employer from the pool.

Side account reports

Number of employers with side accounts (as of December 31, 2024, valuation)

As shown in the table below, 232 employers have established side accounts.

| Employer type | Number of employers with

side accounts |

| State agencies (all, including Oregon University System) | 5* |

| Pooled cities | 29 |

| Pooled community colleges | 17 |

| Pooled counties | 16 |

| Pooled special districts | 23 |

| School Districts Pool | 125 |

| Independent locals (not a member of a pool) | 17 |

*State agencies share a single side account. In addition to this side account, four state agencies have

established individual side accounts.

Number of employers with more than one side account (as of December 31, 2024)

There are no restrictions on the number of side accounts an employer may have.

As of December 31, 2024,90employers have more than one side account; 24 employers have three or more side accounts

| Employer type | Number of employers with multiple side accounts

|

| State agencies (all, including Oregon University System) | 4 |

| Pooled cities | 4 |

| Pooled community colleges | 7 |

| Pooled counties | 5 |

| Pooled special districts | 7 |

| School Districts Pool | 57 |

| Independent locals (not a member of a pool) | 6 |

Side account assets (as of December 31, 2024)

Side account assets totals, by type of employer.

| Employer type | Total side account assets |

| State agencies* |

$697,548,197

|

| Pooled cities |

$54,512,884

|

| Pooled community colleges |

$574,495,483

|

| Pooled counties |

$208,569,142

|

| Pooled special districts |

$166,644,967

|

| School Districts Pool |

$2,348,353,137

|

| State and Local Government Rate Pool |

$1,701,770,673

|

| Independent locals (not a member of a pool) |

$350,121,083

|

*Includes individual side accounts for OSU, SAIF, U of O, and the State Bar Professional Liability Fund

Side account summaries by year

2024 summary

2023 summary

2022 summary

2021 summary

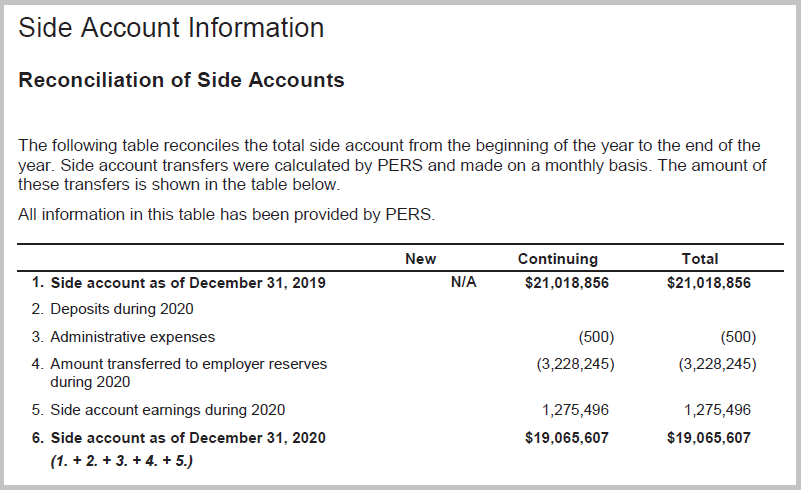

2020 summary

2019 summary

2018 summary

2017 summary

Average earnings by year (from 2007 to 2024)

Side accounts are invested in the PERS Fund and receive the fund's actual earnings or losses. These earnings

or losses are posted to side accounts at the end of each year.

| Calendar year | Average earnings/losses |

| 2007 | 10.22% |

| 2008 | –27.83% |

| 2009 | 19.52% |

| 2010 | 13.13% |

| 2011 | 2.96% |

| 2012 | 15.39% |

| 2013 | 16.67% |

| 2014 | 7.79% |

| 2015 | 2.25% |

| 2016 | 7.65% |

| 2017 | 16.71% |

| 2018 | 0.56% |

| 2019 | 13.92% |

| 2020 | 7.18% |

| 2021 | 18.93% |

| 2022 | -1.85% |

| 2023 | 6.34% |

| 2024 | 6.70% |

Note: These rates are calculated based on the total side accounts balance less administrative

fees.

Pension obligation bonds

Pension obligation bond (POB) requirements

Before issuing a bond

Senate Bill 1049 (2019) expanded the guidelines for employers funding side accounts with pension obligation bonds.

Before issuing a POB, an employer must obtain and submit an assessment as follows:

You must obtain a

statistically based assessment from an independent economic or financial consulting firm to

assess the likelihood that the investment returns on bond proceeds will exceed the interest cost of the

bonds under various conditions.

You must give the assessment to the

state treasurer at least 30 days before issuing the bonds.

You must make a

report available to the public that describes the results of that assessment and discloses

whether you retained the services of an independent SEC-registered advisor.

After issuing a bond

Employers are required to report the following to the state treasurer by December 1 every year.

Other considerations

Pension obligation bond rates of return

To assist employers with this required reporting, PERS is providing the average rate of return for side accounts

in the previous year and the cumulative rate of return as of the current year.

| Year pension obligation bond was established | Actual rate of return on proceeds in previous year | Cumulative rate of return |

| 2020 | 6.71% | 41.97% |

| 2021 | 6.71% | 32.46% |

| 2022 | 6.71% | 11.37% |

| 2023 | 6.71% | 13.47% |

| 2024 | 6.71% | 6.71% |

| 2025 | N/A | N/A |

| Year | Year-to-date average final crediting rate for side accounts |

| 2020 | 7.18% |

| 2021 | 18.93% |

| 2022 | -1.85% |

| 2023 | 6.34% |

| 2024 | 6.71% |

| 2025 | N/A |

Information and assistance

Contact us

If you're interested in establishing a side account or have additional questions, please email

PERS Actuarial Services.

Questions?

Email

actuarial.services@pers.oregon.gov to ask anything about your

side account or to schedule time to go over your options.